818

818

Your SEO dashboard tells a story you’d rather ignore. Organic traffic is down 35% since May. Click-through rates have flatlined despite stable impressions. Meanwhile, Google’s announcing AI features left and right—AI Overviews here, AI Mode there—while their stock soars past $3 trillion.

The real issue? This isn’t just a traffic problem. It’s an economic breaking point disguised as innovation.

Search engines have evolved from basic keyword matching to neural embeddings and conversational queries, culminating in Large Language Models like AI Overviews and AI Mode. However, this evolution faces a market correction driven by unsustainable costs—Google reduced AI Overview operational expenses by 90% within 18 months precisely because the initial model wasn’t viable—forcing a balance between AI innovation and monetization.

- The Historical Evolution of Search: From Keywords to Neural Understanding

- The Current State: Large Language Models Reshape Search

- Market Dynamics: The Forces Shaping Search's Evolution

- Impact on Publishers and Content Creators

- Future Predictions: The Post-Correction Search Landscape

- Alternative Search Engines and the Competitive Landscape

- Conclusion: Navigating Search's Inevitable Transformation

- Frequently Asked Questions

The Historical Evolution of Search: From Keywords to Neural Understanding

The search evolution didn’t happen overnight. Understanding where we’ve been helps predict where we’re headed – especially as AI fundamentally reshapes information discovery patterns.

Twenty years ago, search meant typing exact keywords and hoping your query matched website text. Google’s PageRank algorithm revolutionized this by evaluating link authority, but the model remained keyword-centric.

Then machine learning changed everything. Google’s 2013 Hummingbird algorithm shifted focus from keywords to semantic understanding – grasping intent rather than just matching words. The 2018 BERT update enhanced this by understanding context, enabling Google to interpret nuanced questions like “can you get medicine for someone’s pharmacy.”

Visual elements evolved too. Featured snippets emerged in 2014, providing direct answers at the top of results – a preview of today’s AI Overviews. The “10 blue links” format began fragmenting into specialized results: knowledge panels, local packs, shopping carousels transformed SERPs into multimedia experiences.

Conversational Queries and Intent Signals

Voice search now represents 20% of all Google searches, fundamentally changing query patterns. People don’t speak like they type. Instead of “weather Boston,” voice users ask “What’s the weather going to be like in Boston this weekend?”

This shift toward natural language queries has grown 14% year-over-year, driven by improved voice recognition accuracy and smart speaker adoption. 71% of consumers prefer voice search over typing, citing speed and convenience. Mobile devices account for 27% of voice search activity, making it essential for businesses targeting on-the-go consumers.

Intent signals – the underlying motivations behind searches – became more valuable than demographics. When someone searches “best budget noise-canceling headphones under $100,” they’re signaling purchase intent, price sensitivity, and product category simultaneously. Google learned to decode these signals, matching queries to content addressing specific user needs rather than just keyword presence.

Visual Search Emergence

Google Lens processes 12-20 billion visual searches monthly, a fourfold increase since 2021, driven by younger demographics aged 18-24 who prefer camera-first interactions.

Visual search enables shopping, translation, and information discovery through images. You can photograph a restaurant menu in Tokyo for instant English translations, or snap furniture pictures to find similar items for purchase.

The Current State: Large Language Models Reshape Search

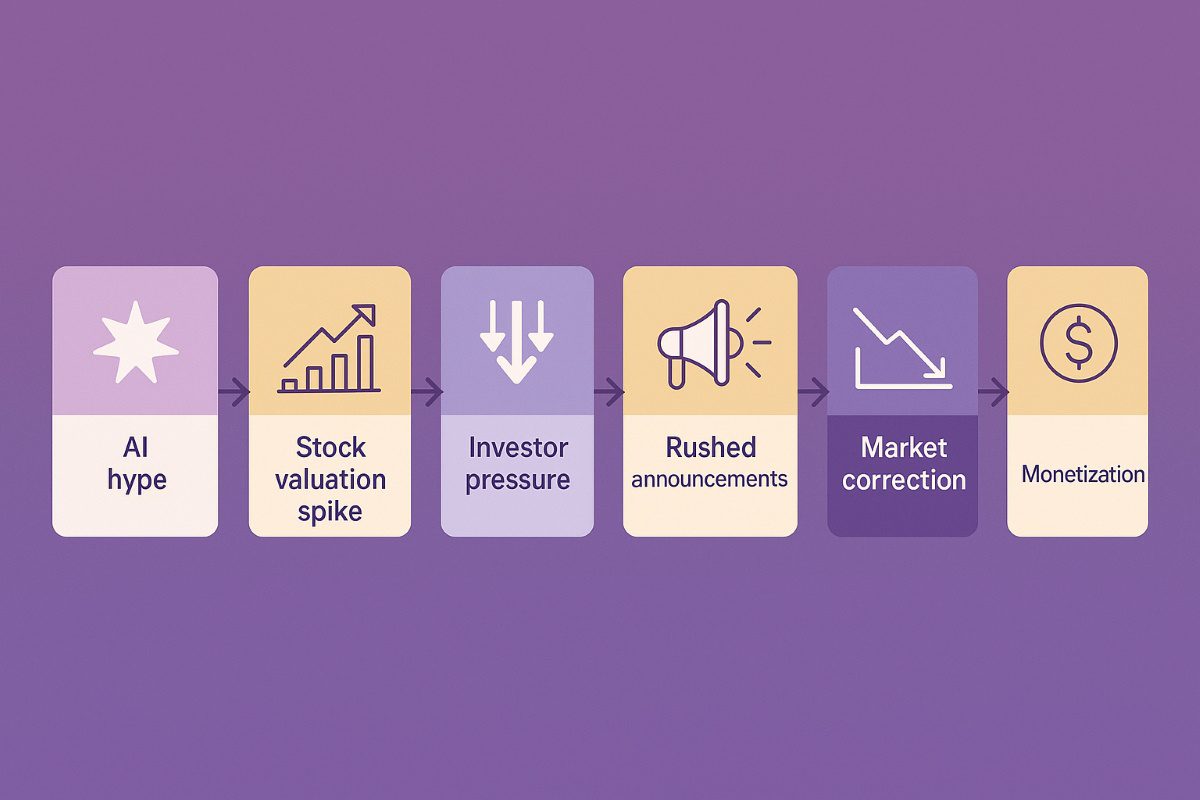

Large Language Models represent the most significant shift in search technology since PageRank. But the path to mainstream LLM integration has been driven as much by competitive pressure and stock valuations as by technological readiness.

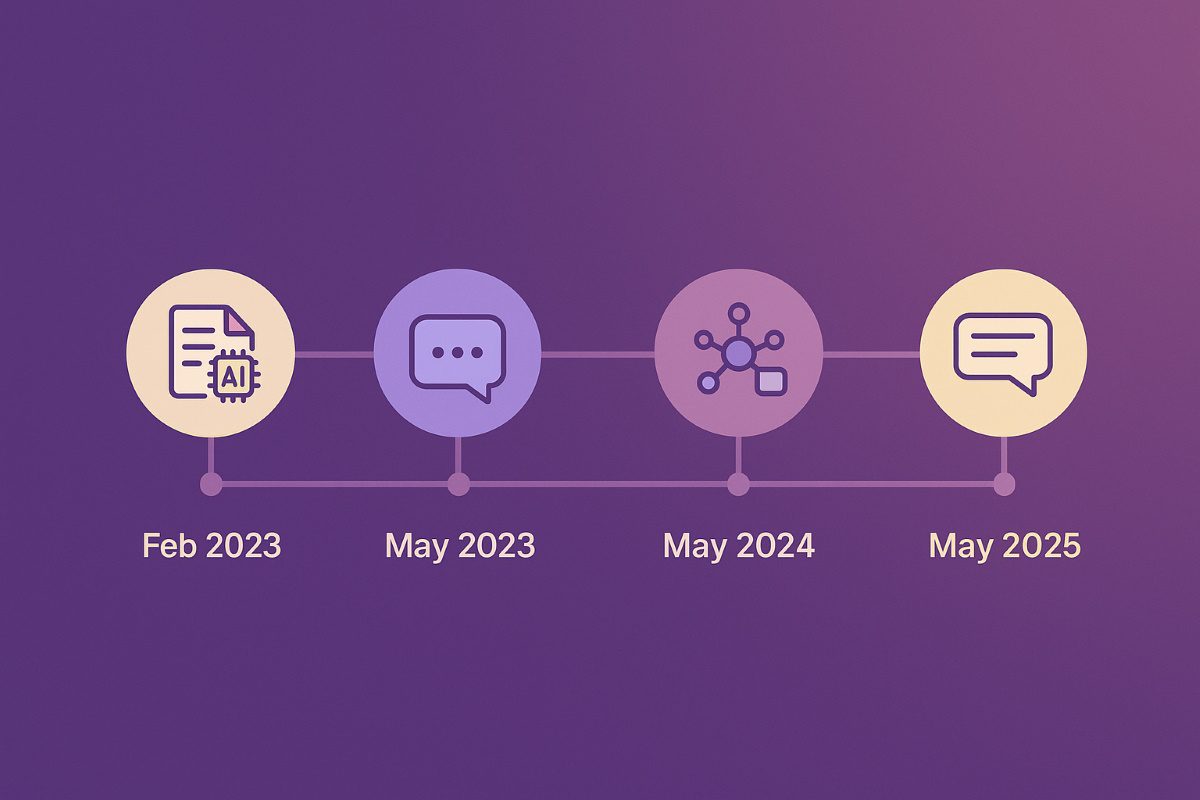

When Microsoft announced Bing’s AI chat in February 2023, it triggered a rapid response from Google. Within a day, Google scrambled to announce “Bard,” setting off a chaotic race to deploy LLMs in search – regardless of whether technology or business models were ready.

Following competitive AI announcements, Alphabet’s stock rose from ~$105-108 per share in early 2023 to $168-186 by late 2024, eventually reaching $3 trillion market valuation by September 2025. Each major AI announcement correlated with stock increases, creating pressure to continually demonstrate AI progress.

This dynamic explains why Google developed two parallel LLM products – AI Overviews and AI Mode – that serve similar purposes. It’s not an optimal strategy; it’s a response to market pressure requiring constant demonstration of AI capabilities.

The sustainability challenge is real. While Google reduced AI Overview costs by 90% over 18 months, researchers estimate AI queries still consume 10x more energy than traditional searches.

AI Overviews: The Interim Solution

AI Overviews (originally “Search Generative Experience”) now appear for 13.14% of all searches, up from 6.49% in January 2025. They provide summaries atop search results, synthesizing information from multiple sources with citations.

Web pages under AI Overviews saw a 34.5% decrease in organic click-through rates, while zero-click searches jumped from 56% to 69% – the “Great Decoupling” Google acknowledged in June 2025.

AI Overviews serve as a gateway experience, integrated directly into search results with no user opt-in required. However, quality issues during initial rollout damaged credibility. Strategically, they’re a transitional product keeping Google competitive while developing something more sophisticated.

AI Mode: Google's True Vision for Search's Future

AI Mode launched for all US users in May 2025 at Google I/O, then expanded to 180+ countries by August. It represents Google’s actual vision for AI-powered search – a conversational interface powered initially by Gemini 2.5 and now Gemini 3.

Liz Reid, Google’s Head of Search, positioned AI Mode clearly: “This is the future of Google search, a search that goes beyond information to intelligence.” Unlike AI Overviews’ summary format, AI Mode enables multi-turn conversations, complex reasoning, and deeper research through a dedicated interface.

The technical capabilities are impressive. AI Mode uses “query fan-out” – breaking questions into subtopics and issuing multiple searches simultaneously. For deep research, it can perform hundreds of searches and create comprehensive reports within minutes.

However, AI Mode is expensive to run and has no monetization model. It’s free in supported regions, competing directly with ChatGPT’s paid subscriptions. This isn’t sustainable, which explains why it remains separate from core search.

Comparison: AI Overviews vs AI Mode

| Feature | AI Overviews | AI Mode |

|---|---|---|

| Cost | Very High (but 90% reduced) | High |

| Quality | Error-prone, improving | Superior reasoning |

| Format | Summary + citations | Dynamic multimodal |

| Integration | Embedded in search results | Separate tab/interface |

| Strategic Role | Interim gateway | Long-term platform |

| Availability | Rolled out globally | 180+ countries, expanding |

Market Dynamics: The Forces Shaping Search's Evolution

Stock valuations, competitive pressure, and unsustainable economics are driving search evolution as much as technological capability. Understanding these forces explains current product decisions and predicts future corrections.

The AI hype cycle has been extraordinary. Alphabet stock surged 50% in 2025 on AI announcements, with each major unveiling correlating to stock increases. This created a loop: AI announcements drive prices, pressuring executives to announce more capabilities regardless of readiness.

Microsoft’s Bing integration with OpenAI triggered this dynamic. Google couldn’t allow Microsoft to claim AI leadership, scrambling to announce competing products even if unpolished.

Google increased capital expenditures to $91-93 billion for 2025, primarily for AI infrastructure: servers, data centers, networking equipment. These aren’t sustainable expense levels without corresponding revenue growth.

The Gartner hype cycle helps contextualize this moment. We’re past “Peak of Inflated Expectations” and entering the “Trough of Disillusionment” where LLM limitations become apparent. The sustainability crisis will force a “Slope of Enlightenment” where realistic, monetizable AI applications emerge.

The Sustainability Crisis: Why Current Models Can't Last

Let’s be direct about the economics: LLM-powered search queries consume approximately 10x more energy than traditional searches. Even with Google’s impressive 90% cost reduction, the operational expenses for serving billions of AI-powered queries daily remain substantially higher than traditional search.

The monetization challenge is clear. Google’s revenue model depends on ad clicks. But AI Overviews and AI Mode reduce click-through rates by providing direct answers. Zero-click searches rose to 69%, meaning users get answers without visiting websites – exactly where advertisers want to reach them.

Google has announced testing ads within AI Overviews, but strategy remains unclear. Users don’t click AI-generated content at rates comparable to traditional results. Early indicators suggest low engagement – explaining why Google hasn’t aggressively monetized these features.

ChatGPT’s pricing offers a preview of inevitable changes. OpenAI charges $20/month for Plus and $200/month for Pro, recognizing unlimited free LLM access isn’t sustainable. Google will eventually need similar monetization through limited free queries, interstitial ads, tiered pricing for power users, or reduced AI response depth for free tiers. The timing depends partly on ChatGPT’s positioning.

Impact on Publishers and Content Creators

The traffic decline for publishers has been swift and significant. Many sites report 30-40% drops in organic traffic after AI Overviews rolled out in their markets. The “Great Decoupling” – rising impressions but falling clicks – means content appears in search results, but users don’t visit websites.

This isn’t just a technical SEO challenge. It’s an existential question for content-driven businesses: if AI provides satisfactory answers directly in search results, what incentive remains for users to click through? The ad-supported web depends on traffic, and AI Overviews fundamentally disrupt this model.

However, declaring “SEO is dead” misses crucial nuances. First, the current situation isn’t sustainable for Google either – the cost structure requires eventual changes. Second, AI search tools rely on high-quality web content for training and responses. If content creation becomes economically unviable, LLMs lose their information source.

The market correction will restore partial traffic patterns. As Google adds exploration features to AI Mode and shifts toward hybrid answer-plus-discovery models, quality content will regain visibility. The key is understanding which content types AI can satisfactorily answer (basic factual queries) versus those requiring human expertise, nuanced analysis, or up-to-date information (where websites remain valuable).

Smart publishers are adapting by:

- Creating depth impossible for AI to replicate: Original research, proprietary data, expert analysis.

- Focusing on topics requiring current information: News, market analysis, real-time updates.

- Building direct audience relationships: Email lists, communities, apps that bypass search dependency.

- Optimizing for AI citations: Structured content that LLMs reference and link to.

Lead Craft’s enterprise SEO services address this challenge through technical audits identifying optimization opportunities in the AI-driven landscape and intent-driven content strategies that capture queries AI tools can’t satisfactorily answer alone. Rather than fighting against AI’s role in search, the focus is on adapting content architecture and authority signals to maintain visibility across traditional search, AI Overviews, and emerging discovery platforms – building sustainable organic growth strategies that reduce paid ad dependency while preparing for market corrections ahead.

Future Predictions: The Post-Correction Search Landscape

The current AI-in-search model will evolve through predictable phases driven by economic reality rather than technological possibility.

- Phase 1: Hype Decrease and Valuation Pressure (6-12 months) As the limitations of LLMs become more apparent – hallucinations, outdated information, lack of reasoning – and as costs remain stubbornly high despite optimization, investor enthusiasm will moderate. Stock valuations tied to AI announcements will face pressure to demonstrate actual revenue growth, not just feature releases.

- Phase 2: Monetization and Limited Free Access (12-24 months) Google will implement restrictions on AI Mode usage for free users. Expect daily query limits (similar to ChatGPT), interstitial ads between queries, or premium subscriptions for unlimited access. This shift will be framed as “ensuring sustainable AI development” while maintaining free access for “most users.”

- Phase 3: Exploration Features and Traffic Rebalancing (18-36 months) Rather than purely answer-focused AI, search will evolve toward hybrid exploration models. AI provides initial context and understanding, then surfaces relevant content for deeper investigation. This approach reduces computational costs (shorter AI responses), provides monetization opportunities (traditional ad placements alongside exploration options), and addresses publisher concerns by restoring some traffic.

Sundar Pichai’s comments hint at this direction: “I think part of why people come to Google is to experience that breadth of the web and go in the direction they want to.” This framing suggests Google recognizes pure answer-generation isn’t the complete solution – users value exploration and discovery beyond single responses.

The Return of Intent-Based Exploration

Intent signals – understanding where users are in their journey – will become more valuable than ever. In an AI-summarized world, how does Google monetize advertising? By understanding user intent deeply enough to target relevant ads at optimal moments.

Currently, AI Overviews bypass much of the traditional ad inventory by providing direct answers. But in exploration-focused models, intent signals enable sophisticated targeting: “User researched X topic through AI, then explored Y category – they’re likely interested in Z products.”

This isn’t hypothetical. Google’s historical emphasis on intent (particularly the 2018 discussions around “micro-moments”) demonstrates the company understands user journeys matter more than individual queries. Monetization requires understanding these journeys to place relevant ads effectively.

Exploration features will likely include:

- Dynamic content portals: AI summaries paired with curated links for deeper investigation.

- Interactive simulations: Google has already previewed generative UI creating visualizations and interactive tools for complex queries.

- Personalized discovery paths: Based on previous searches and interests, suggesting relevant explorations.

- Multi-format results: Video, podcasts, articles, and interactive content surfaced alongside AI responses.

Alternative Search Engines and the Competitive Landscape

While Google dominates with 89-91% market share, the competitive landscape provides context for how search evolution might unfold.

ChatGPT has gained significant attention but remains tiny in actual search volume. Google processes 373x more searches than ChatGPT, with estimates placing ChatGPT’s search market share at less than 1% to approximately 2.1%depending on methodology. Despite impressive growth – 740% increase in 12 months by some measures – the absolute numbers remain small.

Importantly, 93.7% of ChatGPT queries are informational rather than transactional, meaning users research topics but ultimately convert through Google or direct website visits. This pattern explains why ChatGPT hasn’t meaningfully impacted Google’s advertising revenue despite growing usage.

Microsoft Copilot (formerly Bing Chat) holds approximately 4% market share, primarily through default browser settings and Microsoft product integration. It’s credible competition in enterprise contexts where Microsoft already dominates productivity tools, but hasn’t broken through with consumers despite OpenAI partnership advantages.

DuckDuckGo maintains 0.73% market share, serving privacy-focused users. It’s not owned by Google (a common misconception) and operates independently, but limited features and network effects prevent broader adoption. The downside: smaller index means less comprehensive results for many queries.

None of these competitors have the resources to sustain free, unlimited access to expensive LLM infrastructure at Google’s scale. This validates the market correction thesis: eventually, economics will force monetization across all AI search tools, leveling competitive dynamics around pricing tiers rather than free access.

Conclusion: Navigating Search's Inevitable Transformation

The search evolution isn’t about AI replacing traditional search – it’s about market forces correcting unsustainable models toward something practical and monetizable.

AI Mode will eventually replace AI Overviews as Google consolidates its LLM products. This transition will be driven by stock valuation pressure giving way to profitability requirements. Free LLM access will become limited as operational costs force monetization through tiered pricing, query limits, or ad-supported models.

The sustainability crisis – 10x energy consumption per query even after 90% cost reduction – makes current economics untenable long-term. Google will shift toward exploration features that balance AI summaries with content discovery, restoring some traffic to publishers while reducing computational costs.

For businesses navigating this transformation:

- Focus on intent-rich content that AI can’t fully replace: proprietary research, expert analysis, timely updates requiring human judgment

- Build authority for Knowledge Graph optimization: structured data, entity relationships, citation-worthy content that LLMs reference

- Optimize for entity relationships rather than just keywords: how does your content connect topics, validate claims, and provide context?

- Develop content AI summaries complement rather than replace: in-depth guides, interactive tools, multi-format resources

The market correction is inevitable – and necessary. What emerges will be more sustainable than today’s unsustainable free-for-all. The winners will be those who understand AI’s role isn’t replacing search, but transforming how people explore information – and who build strategies for both the current AI hype and the coming correction.

Frequently Asked Questions

What are the 5 types of search engines?

The main types include general-purpose search engines (Google, Bing), vertical search engines (YouTube for videos, Amazon for products), metasearch engines (aggregating results from multiple sources), semantic search engines (understanding context and intent), and AI-powered search engines (ChatGPT, Perplexity using LLMs).

What will replace Google search?

No single platform will likely replace Google, which maintains 90%+ market share. AI Mode represents Google’s own evolution, while ChatGPT serves different use cases (conversational research vs. quick answers). The future is specialization: different tools for different query types rather than one dominant platform.

Why doesn't Gen Z use Google?

Gen Z increasingly starts searches on platforms like TikTok, Instagram, and Reddit for product discovery and recommendations, preferring video-first and peer-validated content over traditional text results. However, they still use Google for transactional queries and specific information needs – just less exclusively than previous generations.

What is the #1 search engine?

Google remains the dominant search engine globally with approximately 90-92% market share, processing over 13 billion searches daily. Its nearest competitor, Bing, holds roughly 4% share. Google’s dominance is even stronger on mobile devices at 95%+ market share.

Is AI replacing SEO?

AI is transforming SEO, not replacing it. Zero-click searches have increased to 69%, reducing website traffic, but the market correction will rebalance this as monetization requires traffic flow. SEO will evolve to focus on intent signals, entity optimization, and creating content that AI tools reference and complement rather than completely answer.

Will SEO exist in 10 years?

Yes, but dramatically different. As AI tools become monetized through tiered pricing and ad-supported models, traffic patterns will partially restore. SEO will focus on authority building, entity relationships, and creating content impossible for AI to fully replicate – original research, expert analysis, proprietary data – rather than basic informational content AI can summarize.

What's the best replacement for Google?

It depends on your needs: ChatGPT excels at conversational, explanatory queries requiring reasoning; DuckDuckGo offers privacy-focused searching; Perplexity provides research-oriented responses with citations. For most commercial and local searches, Google remains superior due to comprehensive indexing, real-time updates, and local business integration.

Share

Share

X

X

LinkedIn

LinkedIn